The global rare earth elements (REE) market is situated at a critical nexus, characterized by immense demand driven by global decarbonization efforts but structurally constrained by extreme supply chain concentration.

The global rare earth minerals market has transitioned from a specialized industrial niche into a primary instrument of statecraft and the fundamental bottleneck for the twenty-first-century energy transition. As of 2025, the market is defined by an unprecedented struggle for strategic autonomy, as Western economies attempt to dismantle a three-decade-old Chinese monopoly.

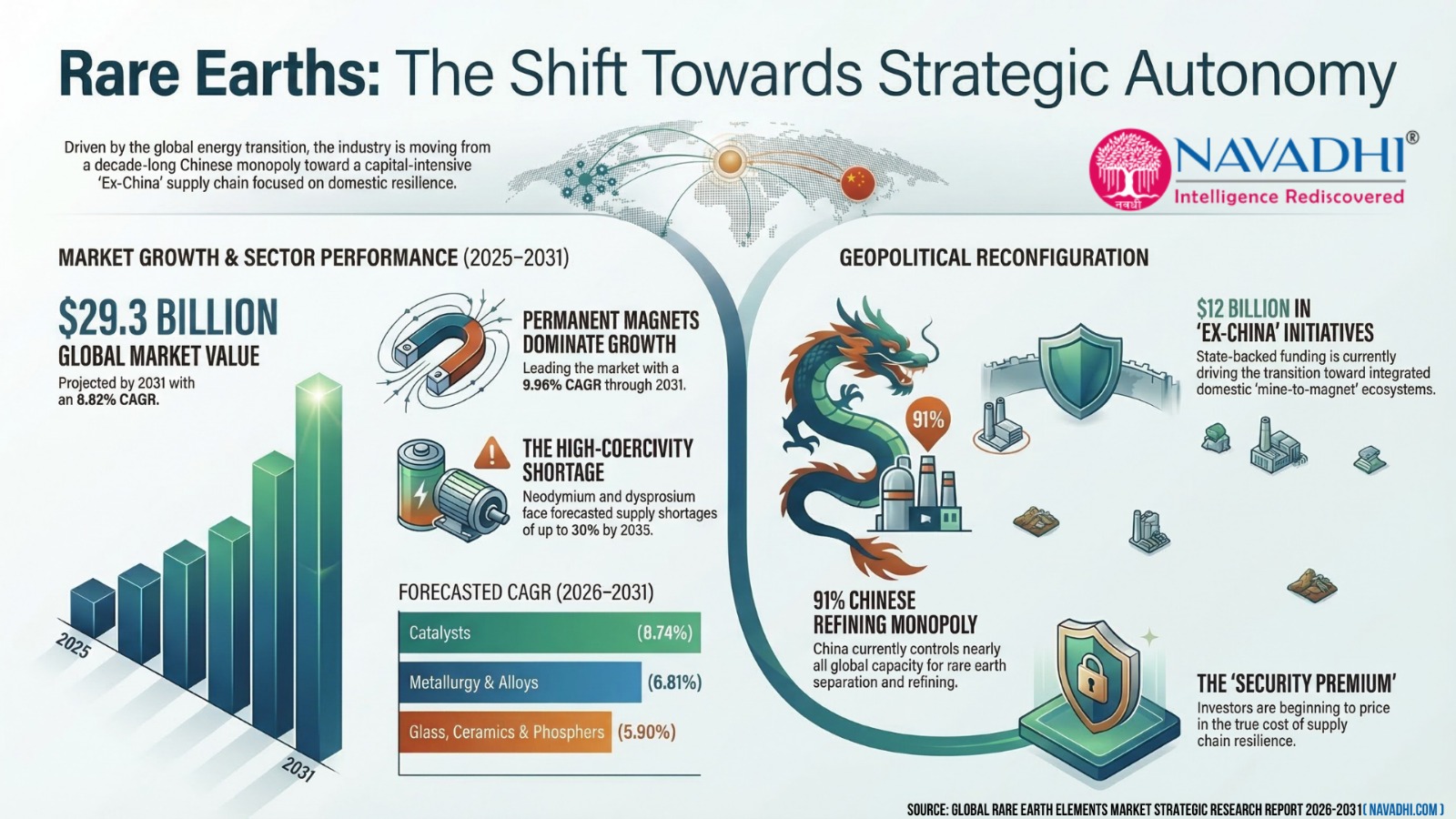

The "Big 3" findings of this analysis underscore a market in high-velocity transformation.

As per this report, the global rare earth elements (REE) market which was worth USD 17.6 billion in 2025 is expected to grow at a CAGR of 8.82% between 2026 and 2031. The global rare earth elements (REE) market is expected to be worth 29.30 billion by 2031.

These estimates were derived using industry strand or measuring the market size based on rare earth oxide (REO) demand forecasts since mines, countries, and companies use Total Rare Earth Oxide (TREO) as standardized unit of measurement in the industry.

As per this research report, the permanent magnets segment which has the highest market share in the global rare earth elements (REE) market is expected to maintain its leadership even in 2031 by growing at the highest CAGR of 9.96% during the forecast period 2026-2031. This is largely due to growing demand for EV motors, robotics and wind turbines.

The catalysts segment is expected to grow at a CAGR of 8.74% till 2031 driven by steady demand from petroleum refining catalysts and emissions control areas.

The metallurgy & alloys segment is expected to grow at a CAGR of 6.81% till 2031 driven by steady demand from aerospace alloys, specialty metals areas which are affected by demand from aviation and space industries.

The glass, ceramics & phosphors segment expected to grow at a CAGR of 5.90% till 2031 driven by consistent demand from niche applications areas like displays, optical glass, specialty ceramics.

For institutional investors and industrial OEMs, the bottom-line opportunity lies in securing physical offtake agreements with these emerging Western refiners, as the market begins to price a "security premium" for non-Chinese materials that reflects the true cost of supply chain resilience.

This forecast is fundamentally reliant on the continued, massive flow of capital into securing non-Chinese supply, as the market value is influenced by extreme price volatility.

The primary strategic imperative defining the industry is the urgent need for decoupling from the Chinese monopoly, which currently controls approximately 91% of global separation and refining capacity. This overwhelming control over the midstream value chain represents the single greatest risk to the stability of energy, electronics, and defense sectors globally. Consequently, government intervention and state-backed diversification efforts are the key catalysts for growth for the global rare earth elements (REE) market.

This research report is ideal for people who wish to gain a thorough understanding of the rare earth elements (REE) market. Some of intended user for this report are:

*If Applicable.

![]()

NAVADHI is a market research company that helps global firms differentiate themselves, break market entry barriers, track their investments, develop business strategies and plan for future by providing actionable market research intelligence that helps them succeed.