The global petrochemical industry has transitioned rapidly from a cyclical slowdown in 2024–2025 to a geopolitical supply shock in 2026, driven by the Iran conflict and disruption of critical trade routes.

The Strait of Hormuz-through which a significant portion of global petrochemical trade flows-has been severely disrupted, impacting shipments of polyethylene, polypropylene, methanol, and fertilizers.

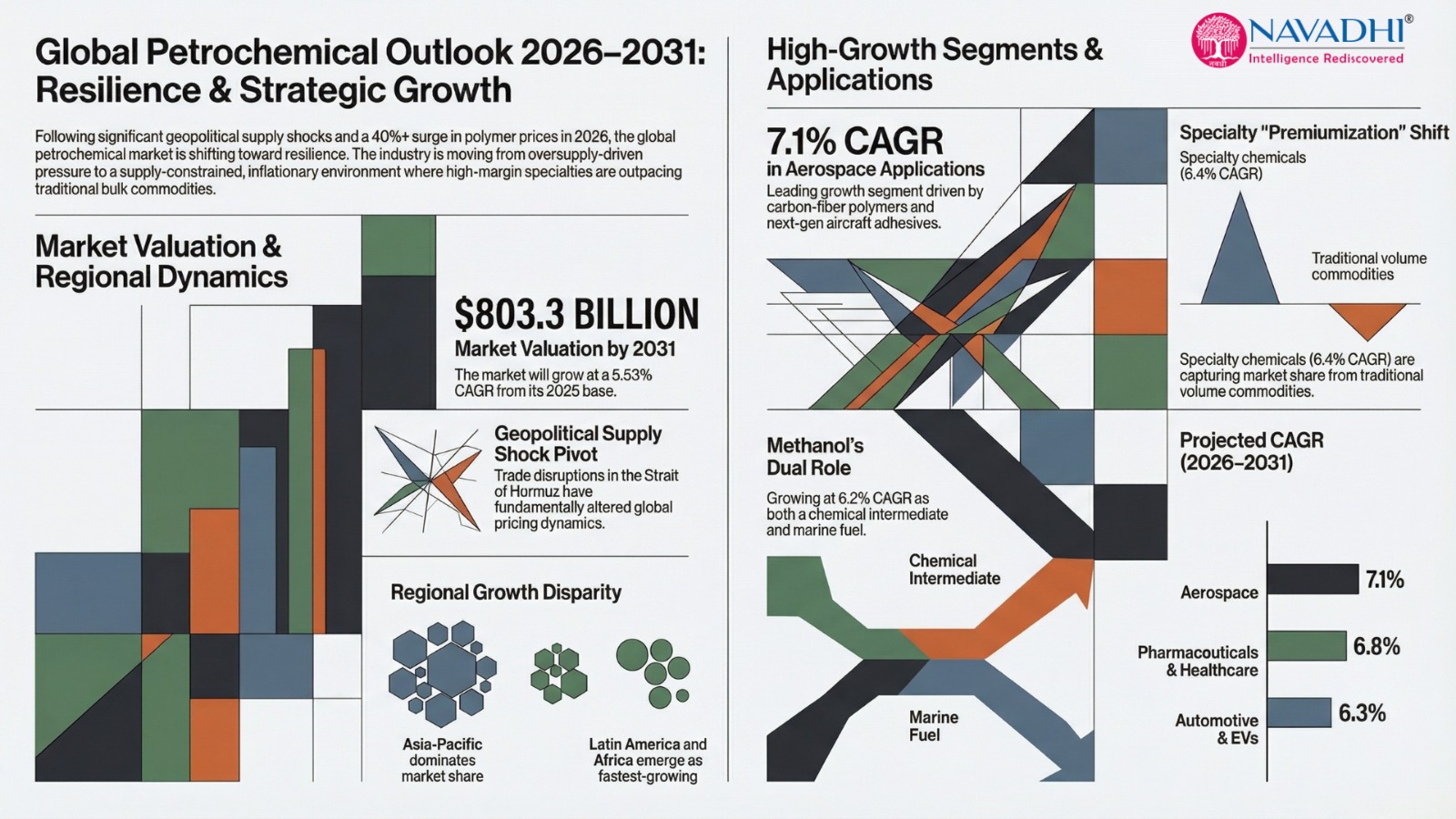

Polymer prices have surged by ~40%+ in some markets. Packaging costs have risen 20%+ due to Polyethylene (PE) / Polypropylene (PP) inflation. Companies such as Dow and peers have implemented aggressive price hikes to pass through costs.

Naphtha and gas supply constraints are affecting Asia and Europe disproportionately. Production outages (e.g., methanol, polymers, LNG-linked chemicals) have emerged in the Middle East.

The industry has shifted from oversupply-driven margin pressure to supply-constrained inflationary environment, fundamentally altering pricing dynamics.

As per this report, the global petrochemical market which was worth USD 582 billion in 2025 is expected to grow at a CAGR of 5.53% between 2026 and 2031. The global petrochemical market is expected to be worth USD 803.30 billion by 2031.

The Asia-Pacific region dominates the global petrochemical landscape and maintains its leadership through the forecast period. Latin America and the Middle East & Africa stand out as the fastest-growing regions, albeit from smaller bases. Europe faces structural headwinds from elevated energy costs, while North America retains a competitive gas-based feedstock advantage.

Ethylene and Propylene collectively account for nearly 46% of the global petrochemical market in 2025, cementing their position as the foundational olefins underpinning downstream plastics, resins, and chemical intermediates. Methanol is the fastest-growing named segment at 6.2% CAGR, reflecting rising demand for methanol-to-olefins (MTO) routes in China and methanol's emerging role as a marine fuel. The 'Others' category - encompassing specialty chemicals, acrylics, and downstream intermediates - grows at ~6.4% CAGR and increases its share from 18.6% to 19.5%, signalling a structural mix-shift toward higher-margin specialties.

Ethylene is the largest segment in global petrochemical market at 27.8% share and is expected to grow at a 5.5% CAGR during 2026-2031, anchored by polyethylene demand in packaging and consumer goods which is consistent with Dow's ethylene value chain representing around 60% of its USD 44.6 Bn sales base.

Propylene is expected to record a CAGR growth of 5.4% during the 2026-2031 period, which shows stable growth.

Benzene / BTX Aromatics segment is expected to grow at 4.8% and face competitive pressure from bio-based substitution in downstream PET and nylon markets, particularly in Europe post-2027.

Methanol is expected to show the highest CAGR growth at 6.2% CAGR during the forecast period, driven by methanol-to-olefins (MTO) capacity in Asia and its emerging dual role as a marine fuel and hydrogen carrier, supported by OCI N.V. and Methanex capacity guidance.

Xylene / Toluene segment is expected to grow at a CAGR of 5.1% during the forecast period.

Butadiene is expected to record slowest growth at 4.4% CAGR, reflecting structural moderation in synthetic rubber demand as EV penetration reduces need for traditional tyre formulations over the long term.

The 'Others' segment encompassing specialty chemicals, acrylics, and downstream intermediates like polyurethane intermediates, and electronic chemicals is expected to grow fastest at 6.4% CAGR and increase its share from 18.6% to 19.5%, adding around 48 billion over the period, signaling a structural mix-shift toward higher-margin specialties.

Packaging is the dominant segment by application at 35% of the total market in 2025, though its share moderates slightly to 34.4% by 2031 as high-growth specialty segments gain relative importance. The packaging petrochemical segment is expected to grow at a CAGR of 5.2% during 2026-2031.

Building & Construction petrochemical segment which has second largest market share in the global petrochemical market is expected to grow at 5.4% CAGR and retain its market share till 2031 mainly due to LyondellBasell's Advanced Polymer Solutions providing a commercial anchor and urbanisation trends in Asia and Middle East which will drive volume.

Automotive & EVs petrochemical segment is expected to register the growth of 6.3% CAGR till 2031 due to EV-driven demand for battery separators, thermal management polymers, and lightweighting composites providing a structural +1.5pp growth premium vs. the prior cycle.

Agriculture / Fertilizers petrochemical segment is expected to record slowest growth at 4.5% CAGR till 2031 reflecting tighter nitrogen fertilizer margins, some crop nutrient substitution trends, and policy-driven efficiency mandates in key agricultural markets.

Consumer & Industrial Goods petrochemical segment is expected to grow at a CAGR of 5% while textiles / synthetic fibers petrochemical segment will grow at 5.5% during 2026-2031.

Pharmaceuticals & healthcare petrochemical segment is expected to grow second fastest at 6.8% CAGR till 2031 due to benefits from expanding biopharma manufacturing globally, rising demand for high-purity chemical intermediates, and health infrastructure build-out in emerging markets.

Aerospace petrochemical segment is expected to record highest CAGR growth at 7.1% in the global petrochemical market, albeit from the smallest market share of 2% in 2025, driven by commercial aviation recovery and increased use of carbon-fibre reinforced polymers and specialty adhesives in next-generation aircraft.

This report identifies emerging market industrialisation & polymer demand, packaging industry expansion & e-commerce surge, automotive lightweighting & ev material transition, north American shale gas feedstock advantage, middle east crude-to-chemicals integration wave, specialty & high-performance polymer premiumisation, circular economy & chemical recycling scale-up, construction & infrastructure boom in South/South East Asia and government policy & sovereign industrial mandates as nine key growth drivers for the global petrochemical market during the forecast period of 2026-2031.

Structural overcapacity - china-driven supply glut, US-China tariff escalation & trade war impact, crude oil & feedstock price volatility, plastic regulation & single-use bans (EU, global), Europe deindustrialisation & energy cost crisis, bio-based & green chemistry substitution risk, EV adoption reducing downstream fuel-chemical co-production, permitting delays & environmental regulatory headwinds and weak consumer demand & global economic slowdown risk were identified as the nine key growth inhibitors / key pain areas affecting the global petrochemical market during the forecast period of 2026-2031.

This research report is ideal for people who wish to gain a thorough understanding of the petrochemical market. Some of intended user for this report are:

*If Applicable.

![]()

NAVADHI is a market research company that helps global firms differentiate themselves, break market entry barriers, track their investments, develop business strategies and plan for future by providing actionable market research intelligence that helps them succeed.