The global peptide active pharmaceutical ingredient (API) market is experiencing transformational growth, driven primarily by the explosive demand for GLP-1 receptor agonists used in diabetes and obesity treatments.

This report covers the full spectrum of peptide active pharmaceutical ingredient (API) across all major global markets for the forecast period 2026–2031, with 2025 as the base year.

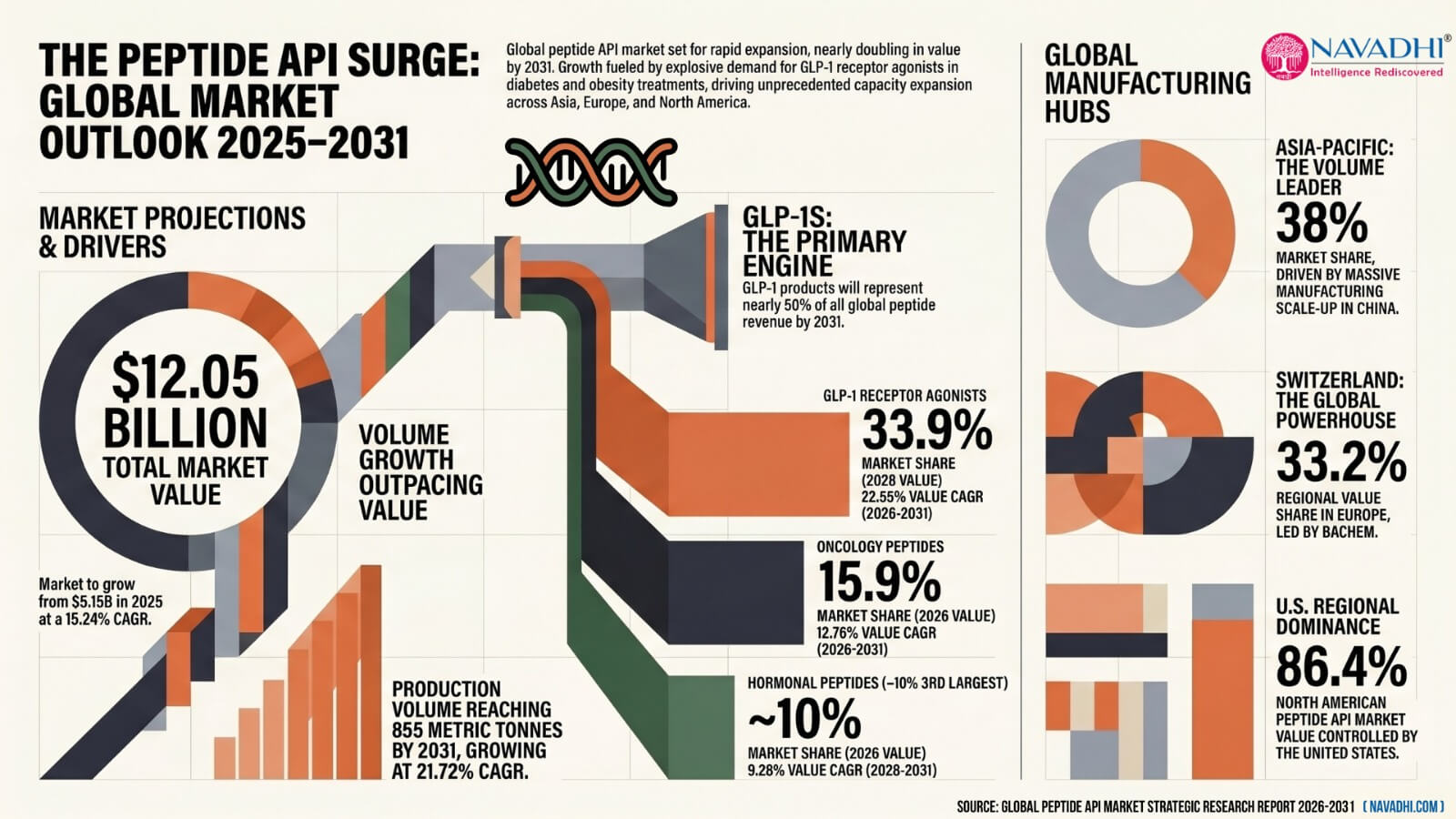

As per this report, the global peptide active pharmaceutical ingredient (API) market which was worth USD 5.15 billion in 2025 is expected to grow at a CAGR of 15.24% between 2026 and 2031 driven primarily by the explosive demand for GLP-1 receptor agonists used in diabetes and obesity treatments. The global peptide API market is expected to be worth USD 12.05 billion by 2031.

The global peptide API market volume which was 265 metric tonnes (MT) in 2025, is expected to grow at a CAGR of 21.72% between 2026 and 20231. The global peptide API market volume is expected to reach 855 metric tonnes (MT) by 2031. This volume growth which outpaces value growth reflects the combination of increased production scale and declining average selling prices as manufacturing matures in the global peptide API market.

GLP-1 Receptor Agonist API are the largest segment type in the global peptide API market at estimated 33.9% market share by value in 2026 and is expected to grow at a CAGR of 22.65% by value and 32.27% by volume during 2026-2031. This segment, encompassing semaglutide, liraglutide, and tirzepatide, is the primary engine of market expansion.

By 2031, nearly half of all global peptide API market revenue will derive from GLP-1 products alone, reflecting the massive therapeutic addressable market for obesity and diabetes medications globally. This explosive growth, particularly between 2022–2024 (27.3% YoY growth), has catalyzed unprecedented capacity expansion and investment across the entire supply chain. Beyond 2025, growth stabilizes to 15.2% annually, reflecting maturation in manufacturing and market penetration rather than a slowdown in underlying drug demand.

Oncology peptides represent the second-largest segment at 15.9% market share by value in 2026 and is expected to grow at a CAGR of 12.76% by value and 19.71% by volume during 2026-2031. This growth of oncology peptides is driven by LHRH analogs for prostate/breast cancer applications.

Hormonal peptides is the third largest segment in the global peptide API market and is expected to grow at a CAGR of 9.28% by value and 16.48% by volume during 2026-2031. The growth hormonal peptides is largely anchored by long-standing products like oxytocin.

Emerging growth comes from CNS/neuropeptides and immunology/rare disease segments, each expanding 10%+ annually, indicating pipeline strength beyond obesity treatments.

The global peptide API market shows stable geographic distribution with Asia-Pacific emerging as the fastest-growing region by volume.

Asia-Pacific with expected 38% value market share in 2026 is estimated to show highest CAGR volume growth at 23.19% driven by China's WuXi STA's 32,000L solid-phase peptide synthesis (SPPS) capacity, GL Biochem, and Hybio Pharmaceutical driving low-cost, high-volume production of GLP-1 APIs.

India's rapidly expanding middle class, and Southeast Asia's emergence as a furniture export hub. China alone contributes approximately 45% of Asia-Pacific's value. Hettich, Hafele, and Blum have all significantly expanded Asia-Pacific manufacturing and distribution.

India peptide API market is expected to see the fastest value growth at 17.97% CAGR during 2026-2031 in Asia-Pacific region driven largely by Piramal Pharma Solutions and PolyPeptide's Ambernath site. Japan (and South Korea are expected to provide specialty and biotech support in the global peptide API market. Asia-Pacific's growth is propelled by cost advantages, GLP-1 manufacturing scale-up, and increasing FDA/EMA compliance.

In North America peptide API market, United States dominates with estimated 86.4% of regional value market share in 2026, anchored by Bachem's manufacturing footprint in California and AmbioPharm's facility in South Carolina. Canada is estimated to contribute 7.9% of value market share in 2026 with growing biotech clusters (Toronto, Vancouver, Montreal). The North America peptide API region benefits from high drug pricing, regulatory proximity, and nearshoring trends.

In Europe peptide API market, Switzerland is expected to remain the global peptide manufacturing powerhouse at estimated 33.2% of regional value market share in 2026, with Bachem (Bubendorf/Sisslerfeld) and PolyPeptide dominating. Germany with estimated 15.9% value market share in 2026 is expected to leverage CordenPharma's Frankfurt facility and emerging capacity at CordenPharma's Basel greenfield for growth. France, Belgium, and the United Kingdom each contribute 7–10%, with PolyPeptide's Strasbourg site and Almac's Northern Ireland facility adding critical capacity. Europe peptide API market's strength derives from decades of manufacturing heritage, regulatory infrastructure, and cluster effects.

In Middle East & Africa peptide API market Saudi Arabia and UAE are developing pharmaceutical hubs (Dubai Science Park, King Abdullah Economic City) supported by healthcare investment.

Brazil dominates Latin America peptide API market with estimated 44% value market share in 2026 via Cristália and Hypera Pharma, benefiting from growing diabetes prevalence.

Consolidation in the global peptide API market is accelerating. Granules India's April 2025 acquisition of Senn Chemicals (Switzerland) signals Indian companies targeting European peptide CDMO capabilities. Bachem's profitability (46.2% gross margin) and strategic positioning around semaglutide give it structural advantage, though scale-up is opening opportunities for well-positioned Asian competitors (WuXi STA, GL Biochem, Hybio) that can absorb high-volume GLP-1 orders.

The global peptide API market is expected to see sustained GLP-1 demand through 2031 with expansion into cardiovascular/CKD indications; manufacturing scale-up staying pace with demand; no major geopolitical disruption of Asian supply; and generic/biosimilar entry post-2031 as patents expire. Companies that succeed will balance volume growth in commoditized segments with margin protection in specialty applications, geographic diversification, and vertical integration.

This research report is ideal for people who wish to gain a thorough understanding of the peptide API market. Some of intended user for this report are:

*If Applicable.

![]()

NAVADHI is a market research company that helps global firms differentiate themselves, break market entry barriers, track their investments, develop business strategies and plan for future by providing actionable market research intelligence that helps them succeed.