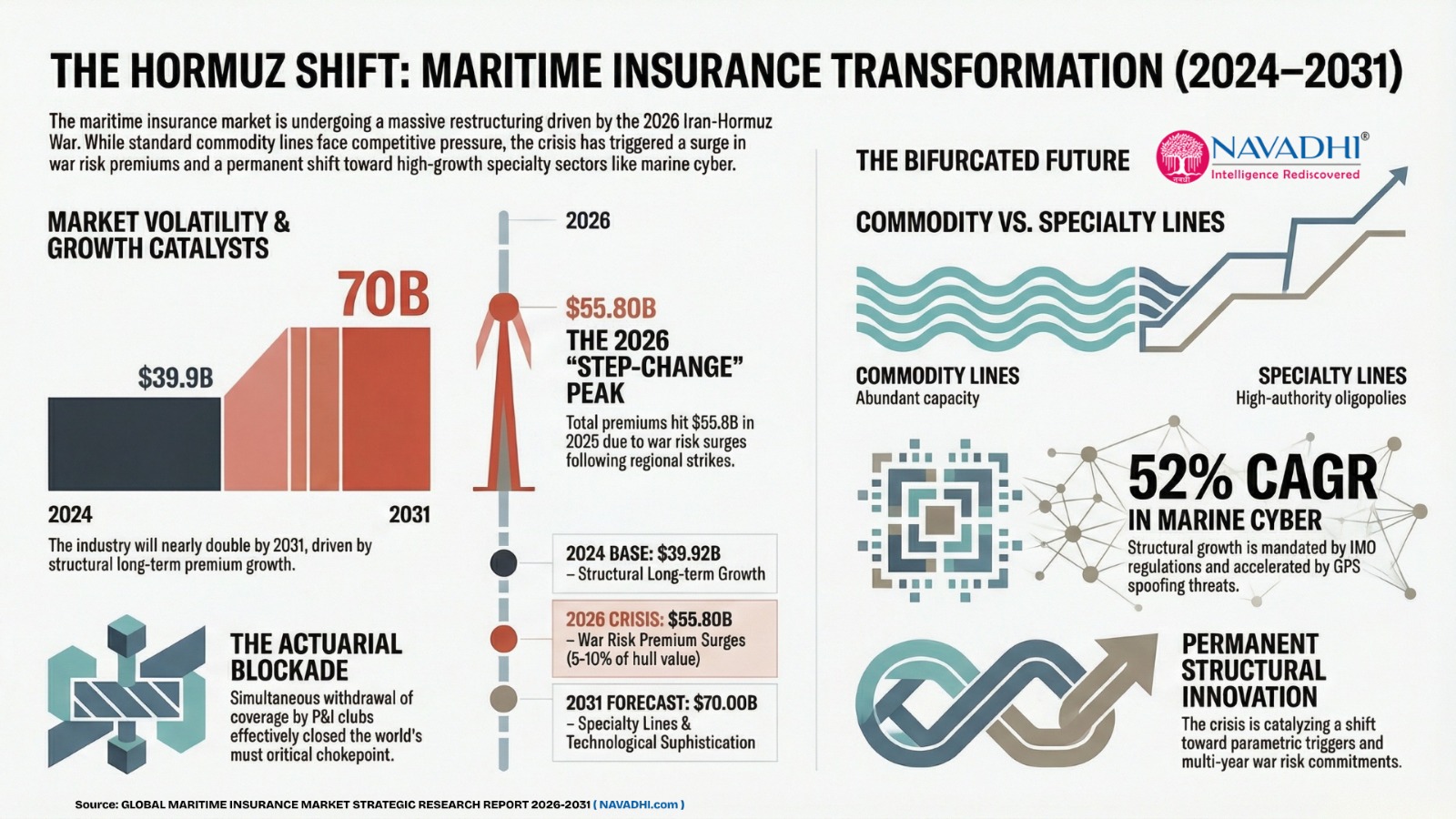

The global maritime insurance market is projected to grow from USD 39.92 billion in 2024 to USD 70.0 billion by 2031, at a blended CAGR of approximately 4.70% under the Base Case scenario - representing the net outcome of structural long-term premium growth, an unprecedented war risk premium surge driven by the Iran-Hormuz War of February 2026, and a gradual post-crisis normalisation through 2027–2028. This growth is neither uniform across product segments nor insulated from material near-term volatility. The 2026 forecast year is the most structurally disrupted in modern maritime insurance history, with total premiums estimated at USD 55.8 billion - a step-change driven by war risk Additional Premiums surging from 0.025% to 5–10%+ of hull value for Hormuz transit coverage within 14 days of the US-Israeli strikes on Iran on February 28, 2026.

The defining characteristic of the 2026–2031 maritime insurance cycle is its bifurcation. Commodity cargo and standard hull markets - accounting for 57% and 24% of global premiums respectively - will experience continued competitive pressure as market capacity remains abundant and pricing discipline is tested by broker-led competition in benign risk environments. Meanwhile, specialty lines - war risk, marine cyber, offshore energy, and P&I liability - operate as constrained-capacity oligopolies where the combination of regulatory approval barriers, actuarial data moats, and reinsurance treaty access creates structural pricing authority unavailable in commodity lines. The Hormuz crisis has crystallised this bifurcation in real time: commodity marine insurers face claims exposure on Gulf-transiting portfolios, while war risk specialists are generating the highest per-policy premium revenues in the industry's modern history.

Marine cyber insurance stands apart as the singular high-conviction growth theme across all scenarios - projected at 52% CAGR from its 2024 base, driven by the Iranian Revolutionary Guard Corps' GPS spoofing operations in the Gulf of Oman during the Hormuz crisis, the IMO's mandatory cyber risk management framework, and the accelerating digitisation of vessel navigation and port management systems. This growth trajectory is not dependent on geopolitical outcomes - it is structurally mandated by regulatory requirements and commercially accelerated by demonstrated threat events.

|

Key Metric |

Value / Detail |

|

2024 Market Size (Confirmed) |

USD 39.92 billion - all-time high; +1.5% on 2023 |

|

2026F Market Size (Base Case) |

USD 55.8 billion - war risk premium surge drives step-change |

|

2031F Market Size (Base Case) |

USD 70.0 billion - structural growth normalises post-crisis |

|

CAGR 2026–2031 (Base Case) |

4.70% - structural premium growth across all lines |

|

CAGR 2026–2031 (Bear Case - Extended Conflict) |

3.40% - prolonged disruption suppresses trade volumes |

|

CAGR 2026–2031 (Bull Case - Rapid Resolution) |

7.90% - pent-up demand surge post-normalisation |

|

Largest Segment 2024 |

Marine Cargo - USD 22.64 billion (57.23% share) |

|

Fastest Growing Segment |

Marine Cyber Insurance - 52.0% CAGR 2026–2031F |

|

War Risk AP Range (March 2026) |

2.5–10%+ of hull value (vs 0.025–0.125% pre-crisis) |

|

Hormuz Transit Collapse (1 Mar 2026) |

81% decline - from ~77 transits/day to ~4 supertanker transits |

|

Largest Geographic Market 2024 |

Europe - ~48.7% of global marine premium |

|

Fastest Growing Region |

Asia-Pacific - 8.2% CAGR 2026–2031F (China = 17.6% of cargo) |

|

IG P&I Clubs Collective Free Reserves |

USD 5.7 billion - all-time high (2024) |

|

Defining Near-Term Risk |

Iran-Hormuz War (Feb 2026) - actuarial blockade mechanism |

The Iran-Hormuz War of 2026 is not merely a short-term premium inflator - it is a market-restructuring event. The 'actuarial blockade' mechanism it demonstrated - whereby seven P&I clubs simultaneously withdrawing war risk coverage effectively closed the world's most critical maritime chokepoint without a single mine or blockade - will permanently alter how shipowners, cargo owners, and regulators structure their insurance arrangements. Multi-year war risk coverage commitments, parametric trigger products, and government-backed war risk facilities are all structural market innovations that the crisis will catalyse through 2027–2028. The maritime insurance market that emerges from the Hormuz crisis will be structurally larger, more premium-intensive, and more technologically sophisticated than the one that entered it.

This research report is ideal for people who wish to gain a thorough understanding of the maritime insurance market. Some of intended user for this report are:

*If Applicable.

![]()

NAVADHI is a market research company that helps global firms differentiate themselves, break market entry barriers, track their investments, develop business strategies and plan for future by providing actionable market research intelligence that helps them succeed.