The global humanoid robotics commercial deployment market stands at a definitive inflection point, representing one of the most consequential emerging technology transitions in modern industrial history.

This report covers the full spectrum of humanoid robotics industry across all major global markets for the forecast period 2026–2031, with 2025 as the base year.

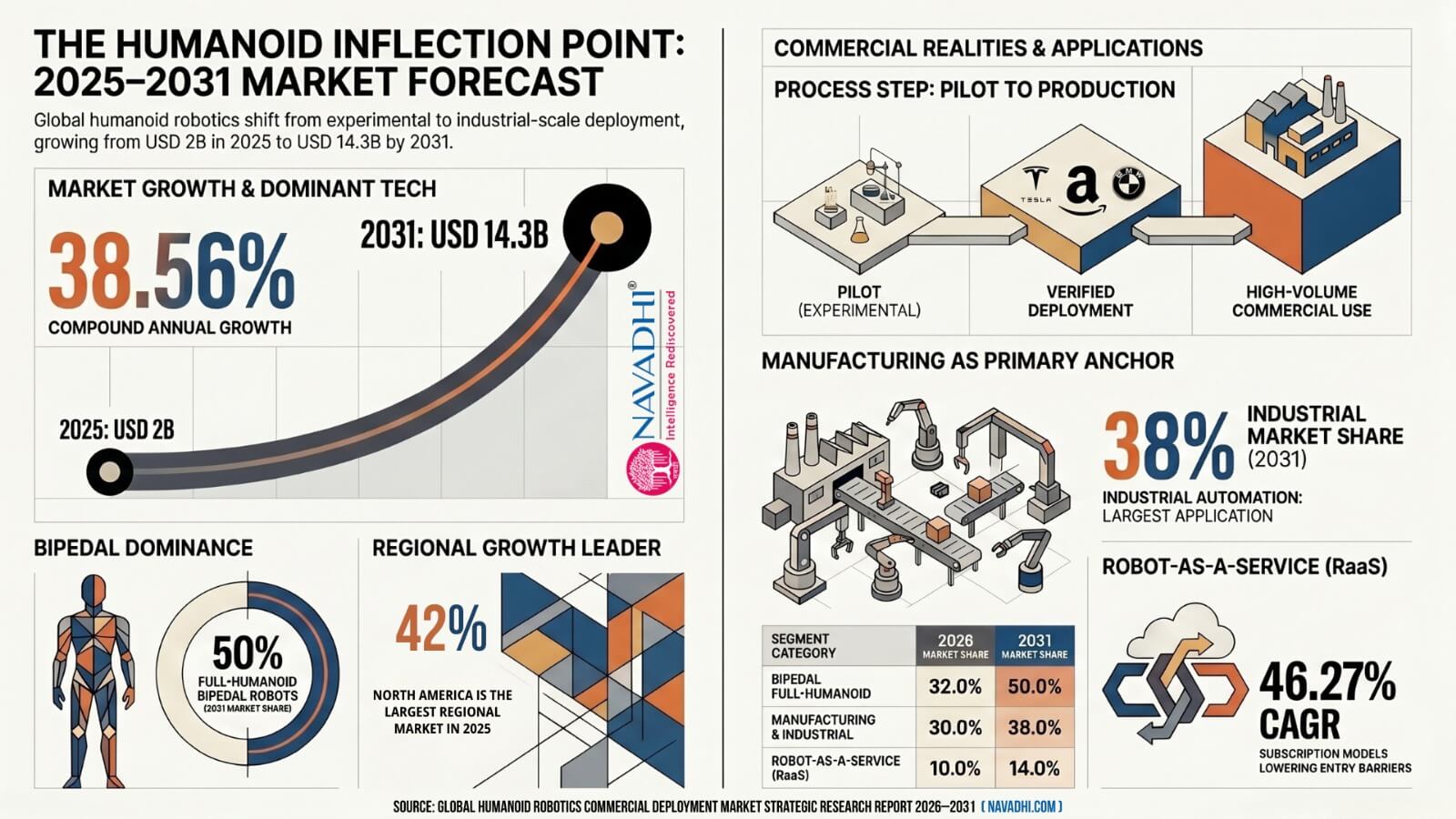

As per this report, the global humanoid robotics market, which was worth USD 2 billion in 2025, is expected to grow at a CAGR of 38.56% between 2026 and 2031. This exceptional growth trajectory reflects the convergence of three decades of advances in AI, actuator technology, power systems, and sensor fusion that are now enabling commercially viable humanoid robots for the first time. The global humanoid robotics market is expected to be worth USD 14.3 billion by 2031.

This expected growth places humanoid robotics among the fastest-growing technology deployment markets globally - comparable in growth dynamics to the early commercialization phases of cloud computing infrastructure and electric vehicle adoption, yet structurally differentiated by its direct substitution economics against human labor across the world's largest employment categories.

The market's ascent is not speculative. It is grounded in verified commercial deployments documented across multiple primary corporate disclosure sources: Tesla's FY2024 Form 10-K confirming approximately 1,500 Optimus units deployed in internal factory operations; Amazon's FY2024 Annual Report confirming Agility Robotics' Digit humanoids operational across Amazon fulfillment center infrastructure; BMW Group's FY2024 Annual Report documenting Figure AI's bipedal humanoid pilot at the Spartanburg manufacturing facility; and UBTECH Robotics' Hong Kong Stock Exchange IPO Prospectus reporting FY2023 revenues of HK$929 million alongside commercial Walker X deployments at BMW Shenyang and Foxconn Shenzhen - representing the first high-volume, documented commercial humanoid deployments at industrial scale globally.

These verified deployment events collectively signal the market's transition from technology demonstration to commercial production - a qualitative shift that fundamentally repositions the risk profile of the humanoid robotics investment thesis.

Bipedal Full-Humanoid Robots is the largest segment type in the global humanoid robotics market at estimated 32% market share by value in 2026 and is expected to grow at a CAGR of 48.8% during 2026-2031 and reach 50.0% market share by 2031. This growth is underpinned by the verified commercial deployments of Tesla Optimus, Agility Digit, Figure 02, and Boston Dynamics Atlas, alongside a cost curve trajectory that projects sub-USD 20,000 pricing for capable bipedal humanoids by the mid-forecast period.

Humanoid Robot-as-a-Service (RaaS) segment anchored by the Moxi subscription model (USD 3,000–5,000 per month), the Agility-Amazon commercial structure, and the Figure AI-BMW pilot arrangement, is estimated to have 10% market share by value in 2026 and is expected to grow second fastest at a CAGR of 46.27% during 2026-2031 and reach 14.0% market share by 2031.

Wheeled and Semi-Humanoid Service Robots segment is expected to grow at a CAGR of 27.43% during 2026-2031. Despite retaining significant absolute revenue growth, this segment is projected to experience relative market share decline from 26.0% to approximately 16.0% as fully bipedal alternatives achieve cost-competitive pricing.

Manufacturing & Industrial Automation is the largest application segment in the global humanoid robotics market at estimated 30% market share by value in 2026 and is expected to grow at a CAGR of 43.99% during 2026-2031 and reach 38.0% market share by 2031. This growth is driven by automotive assembly, electronics manufacturing, and general-purpose factory material handling representing the primary deployment use cases, with verified demand anchors including Tesla's internal Optimus deployment, BMW's Figure AI partnership, and UBTECH's Walker X installations at BMW Shenyang and Foxconn Shenzhen.

Logistics and Warehousing represents the second-largest and second-fastest growing application segment, expected to grow at approximately 43.25% CAGR during 2026-2031. This growth is driven principally by the Amazon-Agility Robotics deployment relationship and the structural imperative of e-commerce fulfillment operators to automate last-touch picking and sorting operations.

Healthcare & Elder Care Assistance application segment, while growing at the comparatively modest CAGR of approximately 31.44% during 2026-2031, represent a long-duration, high-value deployment opportunity as hospital service robot adoption broadens from early adopter academic medical centers to mainstream community hospital systems.

North America is the largest regional market in 2025, representing approximately 42.0% of global market value - a function of U.S.-headquartered leadership across the most commercially advanced humanoid platforms (Tesla, Agility Robotics, Figure AI, Boston Dynamics, Sanctuary AI) and the concentration of high-wage manufacturing and logistics operations that generate the most compelling substitution economics.

However, North America's share is projected to moderate to approximately 35.0% by 2031 as Asia-Pacific - led by China's vertically integrated humanoid robotics manufacturing ecosystem (Unitree, Fourier Intelligence, UBTECH, Agibot) - and the Middle East & Africa region scale rapidly.

The Middle East & Africa is identified as the fastest-growing regional market over the forecast period, at approximately 49.0% CAGR, driven by Saudi Arabia's Vision 2030 industrial automation investments, which underpin that country's status as the single fastest-growing national market globally at approximately 50.0% CAGR.

The global humanoid robotics commercial deployment market has demonstrably transitioned from a technology development phase to an early commercial deployment phase as of 2024–2025. The convergence of embodied AI maturity, actuator cost reduction, compelling labor substitution economics, and verified deployments across leading global manufacturers provides a structurally credible foundation for the 38.8% CAGR forecast through 2031. The market's USD 14.3 billion 2031 projection should be understood as a base-case estimate - one that assumes measured rather than accelerated deployment velocity and reflects a conservative interpretation of Tesla Optimus commercial scale relative to management guidance.

For strategic planners, technology investors, and procurement executives across manufacturing, logistics, and healthcare sectors, the central analytical conclusion of this report is unambiguous: the question of whether humanoid robots will achieve broad commercial deployment is resolved. The operative strategic questions are now when at what scale, at what price point, and by which platform vendors the majority of that deployment value will be captured - and those questions form the analytical core of the detailed segmentation, regional, and competitive analysis contained in the sections that follow.

This research report is ideal for people who wish to gain a thorough understanding of the humanoid robotics commercial deployment market. Some of intended user for this report are:

*If Applicable.

![]()

NAVADHI is a market research company that helps global firms differentiate themselves, break market entry barriers, track their investments, develop business strategies and plan for future by providing actionable market research intelligence that helps them succeed.