The global fertilizer market is transitioning from a post-shock recovery phase into a period of structurally anchored, gradually accelerating growth. The global fertilizer landscape has shifted from a period of "constrained equilibrium" into a state of active structural rupture. As of March 2026, the industry is no longer merely navigating the tailwinds of 2022; it is being forcibly rewired by the March 2026 Iran Conflict, which has surpassed previous benchmarks for geopolitical risk.

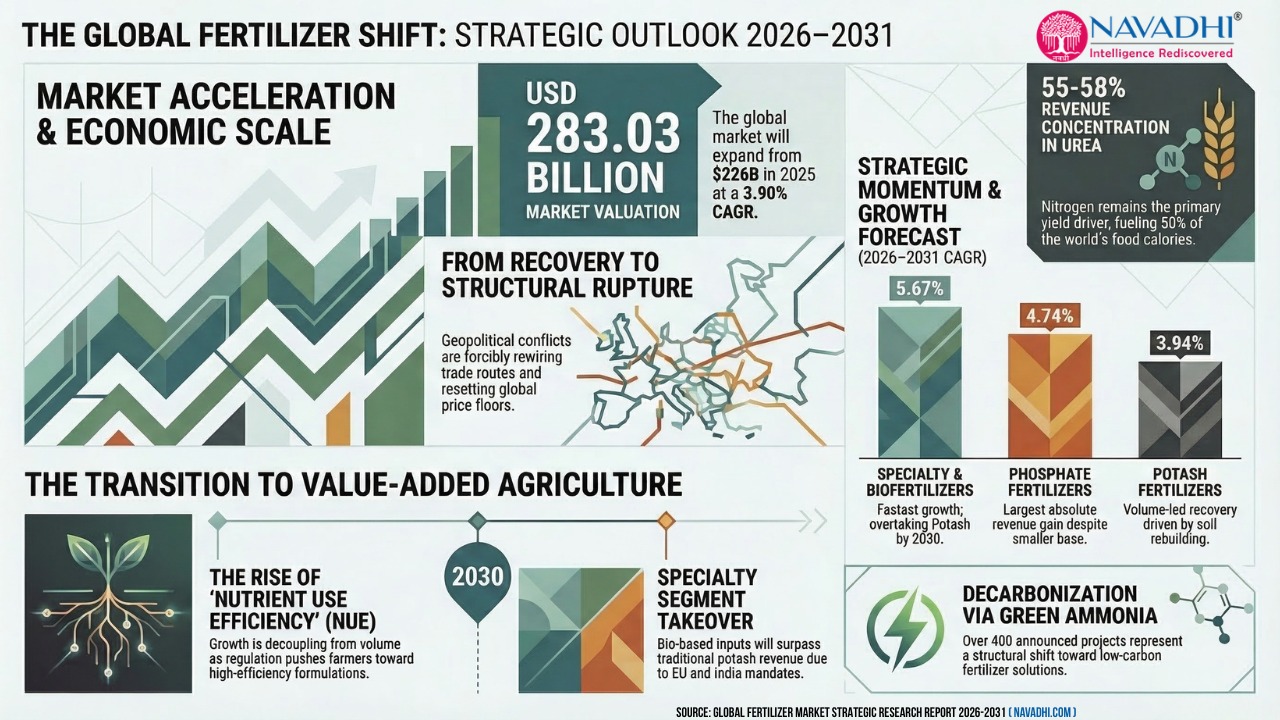

As per this report, the global fertilizer market which was worth USD 226 billion in 2025 is expected to grow at a CAGR of 3.90% between 2026 and 2031. The global Fertilizer market is expected to be worth USD 283.03 billion by 2031.

The global fertilizer market is sized on a standard scope basis encompassing mineral nitrogen, phosphate, potash and compound NPK fertilizers, organic fertilizers, and biofertilizers. Crop protection chemicals, soil amendments, and seed treatments are excluded. Market value is expressed in USD at prevailing FOB (Free on Board)/ CIF (Cost, Insurance, and Freight) prices for each forecast year, reflecting NAVADHI's proprietary price-volume decomposition model.

As per this research report, nitrogen fertilizers constitute the largest segment of the global fertilizer market and will retain that position through 2031, albeit with a declining share of the total market. The global nitrogen fertilizer segment is expected to grow at a CAGR of 2.54% during the forecast period of 2026-2031. It is the lowest among the four segments and reflects a structurally maturing market where volume growth is being moderated by "nutrient use efficiency" (NUE) pressures even as absolute revenue continues to expand.

The primary driver of volume demand remains food calorie production, given that nitrogen (principally as urea) is the single most important yield-determining input for cereals, which provide approximately 50% of global calorie supply. Urea alone accounts for approximately 55–58% of nitrogen fertilizer revenue, with ammonium nitrate, UAN, CAN, and ammonium sulfate comprising the balance.

The global phosphate fertilizers segment which has second largest market share is expected to deliver the largest absolute revenue gain over the forecast period of 2026-2031 despite being a smaller base. The phosphate fertilizers segment is expected to grow at a CAGR of 4.74% which reflects a segment where supply-side structural tightening is the primary pricing driver, compounding on top of solid underlying volume demand growth.

DAP (diammonium phosphate) is the globally dominant product form with approximately 37–46% of phosphate fertilizer revenue, followed by MAP (monoammonium phosphate), TSP (triple superphosphate), and SSP. China, historically the world's largest phosphate exporter and a price-suppressing safety valve for global markets, has systematically restricted phosphate exports since 2021 through quota and licence mechanisms. This structural supply withdrawal - driven by China's desire to retain phosphate resources for domestic food security - has permanently reset the global phosphate price floor. DAP prices rose from approximately USD 336/tonne in early 2024 to USD 437/tonne by May 2025, a 30% increase that flows directly through to segment revenue.

The global potash fertilizers segment is the most volume-sensitive segment, where demand is primarily driven by agronomic necessity i.e. crop potassium uptake rather than by policy incentives or premium-product adoption. MOP (muriate of potash, potassium chloride) accounts for approximately 86% of the potash fertilizer market by value, with SOP (sulphate of potash) occupying the premium niche for chloride-sensitive crops and controlled-environment agriculture.

The global potash fertilizers segment is expected to grow at a CAGR of 3.94% till 2031 and is positioned as a volume-led, moderately price-supported growth segment. The medium-term outlook by International Fertilizer Association (IFA) projects potash consumption growth of approximately 10% between 2024 and 2028 which is the highest volume growth rate among the three macro-nutrients, reflecting crop nutrient depletion rebuilding after the 2022–23 affordability shock caused sharp demand destruction. Brazilian soil rebuilding demand (where potash application rates declined significantly in 2022–23 as prices peaked) is a meaningful recovery driver through 2027.

The global specialty & biofertilizers segment is expected to show the fastest growth at a CAGR of 5.67% till 2031. This report finds that the global specialty & biofertilizers segment is expected to overtake the global potash fertilizers segment by 2030 in terms of overall revenue-based market share which signals the beginning of a structural rebalancing of the fertilizer market away from pure commodity inputs toward value-added, precision, and biological alternatives. This expected growth of the global specialty & biofertilizers segment is mainly attributed to following independently powerful growth forces that are still in their early-to-mid adoption phase –

However, this growth is increasingly decoupled from simple volume expansion; the industry is shifting toward "value-per-nutrient" through precision application technologies, specialty formulations, and digital agronomy.

Geopolitical risks have transitioned from peripheral concerns to central determinants of market stability. The persistent Russia-Ukraine conflict and volatility in the Strait of Hormuz—a corridor handling 35% of global urea trade—have forced a fundamental "structural rewiring" of global trade routes. This has led to a bifurcation of the market: one segment focused on low-cost, resource-heavy production in regions like West Asia and Russia, and another pursuing high-tech, low-carbon solutions in North America and Europe.

Sustainability has emerged as a disruptive force. The expansion of green ammonia capacity, driven by over 400 announced projects, represents a long-term decarbonization. Concurrently, the rise of "nutrient use efficiency" (NUE) as a regulatory and economic priority is fueling the liquid and controlled-release segments, outpacing traditional dry/granular products.

This report identifies population growth & food security imperative, emerging market agricultural intensification, crop price transmission & farmer purchasing power, geopolitical supply tightening - price floor effect, government policy & subsidy support, specialty & biofertilizer premiumisation wave, green & low-carbon fertilizer premium market, precision agriculture - product mix upgrade and ex-china supply chain build-out (sovereign capital) as nine key growth drivers for the global fertilizer market during the forecast period of 2026-2031.

Chinese export control escalation, extreme commodity price volatility, high energy cost sensitivity - nitrogen competitiveness, western permitting & regulatory delay, nano & biofertilizer volume displacement, regulatory volume restrictions (eu farm to fork), russian/belarusian potash re-entry risk, smallholder distribution & affordability gap and climate volatility & demand uncertainty were identified as the nine key pain areas / growth inhibitors affecting the global fertilizer market during the forecast period of 2026-2031.

This research report is ideal for people who wish to gain a thorough understanding of the fertilizers market. Some of intended user for this report are:

*If Applicable.

![]()

NAVADHI is a market research company that helps global firms differentiate themselves, break market entry barriers, track their investments, develop business strategies and plan for future by providing actionable market research intelligence that helps them succeed.